Sure Dividend published this amazing post on the highest-yielding monthly dividend stocks Canada. We have permission to republish it here.

Monthly dividend stocks allow for dividend investors to compound their wealth monthly as opposed to quarterly, which is the most common dividend schedule in the world of investing.

This frequent dividend payment allows for investors to reinvest their money more quickly if they are in the asset accumulation phase of their life, or to cover living expenses for retirees.

You can download our full list of all 50 monthly dividend stocks (along with important financial metrics like dividend yields and payout ratios) by clicking on the link below:

Click here to download your free spreadsheet of all 50 monthly dividend stocks now.

Three years ago, we looked into Three Canadian Monthly Dividend Stocks with Yields Up to 8%. Since then, two of those companies have been acquired. The third company is included once again in this article.

Inter Pipeline Ltd. was fully acquired by Brookfield Infrastructure in late October 2021. Brookfield offered shareholders $20.00 in cash per share, or a quarter of a Brookfield Infrastructure share, or any combination of these. IPL.TO was then delisted from the TSX on November 1st, 2021.

Dream Global REIT was acquired by The Blackstone Group Inc. in an all-cash transaction for $6.2 billion. Each unitholder of DRG.UN received $16.79 per unit.

Below are three Canadian companies trading on the Toronto Stock Exchange which have dividend yields of 5% to 6% and have paid dividends every single month for many years.

Two of the companies below have dividend growth histories spanning over a decade, for income investors who count on dividend growth in addition to yield.

Canadian High-Yield Stock #1: Pembina Pipeline Corp. (PBA)

Pembina Pipeline Corporation is a major provider of transportation and midstream services. Pembina owns pipelines which transport hydrocarbon liquids and natural gas products.

Additionally, they own gas gathering and processing facilities and an oil and natural gas liquids infrastructure and logistics business.

They operate in Western Canada and have served their customers for more than 65 years.

Though Pembina is a Canadian company trading under the ticker PPL on the TSX, it also trades on the NYSE under the ticker PBA.

The company owns and operates three different business segments in western Canada. The three business segments of Pembina consist of: Pipelines, Facilities and Marketing & New Ventures. For FY 2021, these segments made up 45%, 35%, and 20% of the company’s pre-tax profit, respectively.

Source: Investor Presentation

The company’s long-term strategy is to acquire and develop high-quality assets that generate stable and predictable cash flow, while delivering strong returns to shareholders.

Pembina already has a large and established backlog of growth projects. These projects lead management to believe the corporation can grow adjusted cash flow per share by 8%-10% per year.

Given Pembina’s volatile earnings history, we anticipate they could grow adjusted cash flow by about 5% per year over the medium term.

Also, they anticipate raising the dividend rate by 5% per year going forward.

Current Events

To further fuel growth, Pembina entered into an agreement with KKR to combine their western Canadian natural gas processing assets into one single, joint venture entity.

Pembina will own 60% of the new entity, and KKR’s global infrastructure fund will own the other 40%. The new company will also acquire Energy Transfer LP’s last 51% stake in Energy Transfer Canada (ETC).

All in, the value of these assets add up to $11.4 billion CAD.

On February 24th 2022, Pembina reported their Q4 and FY 2021 results. For Q4, adjusted cash flow from operating activities per share rose 21% compared to 2020, from $1.10 CAD to $1.33.

Adjusted EBITDA also grew 12% year-over-year to $970 million.

For the full-year 2021, the corporation grew adjusted cash flow from operating activities per share by 15%, to $4.80.

Adjusted EBITDA was slightly higher compared to 2020, a 5% increase to $3.4 billion.

With adjusted cash flow per share of $4.80, and the FY 2021 dividend payment of $2.52, Pembina achieved a magnificent payout ratio of 53%.

While a safe and stable dividend is of utmost importance to dividend investors, companies committed to increasing the dividend every single year provide even more benefit.

Pembina is one such company as it has paid a higher dividend for ten consecutive years, from $1.56 CAD in 2011 to $2.52 in 2021. Thus, Pembina has increased the annual dividend by 4.9% per year on average over the last decade.

Valuation & Total Returns

Pembina Pipeline is a company where adjusted cash flow (“ACF”) from operations are used to calculate the dividend payout ratio, and it’s one whose valuation can be based on price-to-ACF.

With adjusted cash flow of $4.80 per share and Pembina’s current share price of $46.32 CAD, PPL.TO’s P/ACF is 9.7.

We see fair value for Pembina at around 10.0 times adjusted cash flow from operations.

This increase in valuation could result in a 0.7% annual tailwind to total returns.

With it’s current $2.52 CAD annual dividend, Pembina yields 5.4% (before any dividend withholding taxes for non-Canadians) and pays its dividend monthly.

All in, we believe Pembina has the potential to generate annualized total returns of 10.4% over the next five years.

These returns stem from a 5% growth rate, a 5.4% starting dividend yield, and a potential valuation tailwind of 0.7% per year.

Canadian High-Yield Stock #2: Exchange Income Corporation (EIFZF)

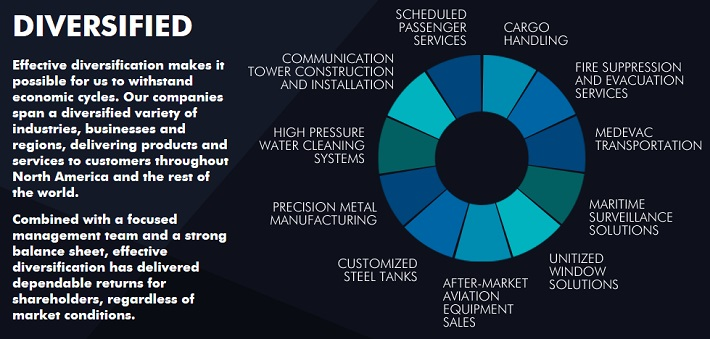

Exchange Income Corporation is a business which makes investments and acquires companies in the aerospace and aviation services and equipment sector, as well as the manufacturing sector.

The companies acquired are in defensible niche markets – medevac transportation, manufacturing of aerospace and defense components, manufacturing of an advanced unitized “window wall system” used primarily in high-rise multi residential developments; the list goes on to the tune of 15 individual operating subsidiaries.

The acquisition candidates must have a track record of profits and strong, continued cash flow generation with their management intact and a commitment to continue building the business.

The strategy of the company is to grow their portfolio of diversified niche operations through acquisition and growth opportunities, and the result of this is to provide shareholders with a reliable and growing dividend.

Source: Investor Relations

The corporation has increased their dividend 14 times in the last 16 years (keeping it stable through year 2009 and 2021), at a 4.8% compound annual growth rate of the dividend.

While a near 5% dividend growth rate is not all that impressive, 14 years of dividend growth bears more weight on the TSX than it does on the NYSE.

This is because Canada has a much smaller list of dividend growth companies, or “aristocrats”.

We expect the company can continue to grow their dividend by about 2.0% over the medium term. This would be supported by an expected adjusted EPS growth rate of about 3.0% per year.

Source: Investor Relations

Current Events

According to their latest quarterly release, payout ratio when calculated as a percentage of free cash flow less maintenance capital expenditures improved to 58% from 71% for the trailing twelve months.

Payout ratio when calculated as a percentage of adjusted net earnings strengthened to 99% from 169% for the trailing twelve months. In addition, the annual dividend payment cost the company 7% more than in FY 2020.

The adjusted net earnings payout ratio indicates the dividend could be at risk and should be monitored.

The company currently pays an annual dividend of $2.28 CAD, which equates to a 5.9% yield at the current share price of $38.85 CAD.

Divided on its monthly payment schedule, that’s a 0.49% return on investment per month before taking any capital appreciation into consideration.

For full-year 2021, Exchange Income generated record high revenue of $1.4 billion, up 23% compared to 2020. Adjusted net earnings improved by 82%, to $86 million.

Adjusted EPS was $2.31 per share for FY 2021, a 71% increase over $1.35 in 2020.

During 2021, EIFZF closed on five acquisitions, a new record for number of acquisitions in a calendar year.

Valuation & Total Returns

We estimate the corporation can generate about $2.56 CAD in adjusted EPS for 2022. Thus, Exchange Income is trading at 15.2 times adjusted EPS.

We see fair value for Exchange Income at around 15.0 times adjusted EPS. This minor valuation drop could result in a (0.2%) annual headwind to total returns.

With it’s current $2.28 CAD annual dividend, EIF.TO yields 5.9%. Combined with our estimated 3% annual EPS growth and marginal valuation headwind, Exchange Income is anticipated to generate annualized total returns of 7.8% over the next five years.

Canadian High-Yield Stock #3: TransAlta Renewables (TRSWF)

In 2013, TransAlta Renewables was spun off from TransAlta (TAC), which remains a major shareholder in the alternative power generation company.

The company’s history in renewable power generation goes back more than 100 years.

Its portfolio is made up of over 45 facilities powered by wind, natural gas, hydro, or solar, in 2022. The corporation generates the majority of its cash flow from its natural gas and wind assets.

Source: Investor Presentation

TransAlta’s portfolio is fortified by long contracts, which is evidenced by its weighted average contract life of more than a decade.

The company has made over $3.5 billion CAD of acquisitions since 2013 but the increase in share count (to fund these acquisitions) has prevented its cash flow per share from rising much, if at all, in certain periods.

For example, TransAlta generated $1.34 CAD in FFO per share in 2013, and in 2021 they posted $1.34 in FCF per share, basically unchanged. From 2012 to 2021 though, its FCF per share increased by about 1.2% per year in USD.

Looking ahead, we think that growth will face a headwind from the Kent Hills 1 and 2 wind facilities outage, as the costs of replacement and foregone revenue will have an impact.

At this time, we estimate TransAlta Renewables can grow FCFPS by about 3% through 2027.

Current Events

About the wind facilities outage, the company recently suffered a tower collapse at the Kent Hills 2 wind site, and upon further investigation, determined that all 50 turbine foundations at the Kent Hills 1 and 2 wind sites require a full foundation replacement.

This rehabilitation will take until the end of 2023 to be fully complete. And the replacement is expected to cost between $75 million and $100 million.

TransAlta Renewables reported fourth quarter and FY 2021 results on February 24th. The company generated slightly less renewable energy production in 2021 at 4,332 GWh compared to 4,471 GWh in 2020.

Still, revenues came in higher by 8% over the prior year, to $470 million CAD.

Year-over-year, adjusted EBITDA was unchanged and FCF dropped 5% to $357 million CAD compared to $377 million. Cash available for distribution (“CAFD”) per share, as a result, also decreased 10% to $1.03 CAD.

Valuation & Total Returns

The company currently pays an annual dividend of $0.94 CAD (paid monthly at $0.07833), which equates to a 5.1% yield at the current share price of $18.57 CAD.

TransAlta Renewables has maintained this dividend rate since 2017, after a series of dividend increases.

We estimate the corporation can generate about $1.26 CAD in FCF for 2022. Thus, TransAlta Renewables is trading at 14.7 times FCF.

We see fair value for the corporation at around 13.0 times FCF. This potential headwind to the valuation could result in a (2.5%) annual loss to total returns.

This valuation headwind, combined with the 5.1% starting dividend yield and 3.0% annual growth in FCF could lead to annualized total returns of 5.1% over the next five years.

More Articles From Wealthy Living Partners

- Best 5G Stocks That Should be on Your Watchlist

- Essential Things You Should Know About Biden’s First Time Home Buyer Grant Program

- Warning Signs a Big Housing Market Crash is Just Around the Corner

- Dividend Kings Stocks That You Should Add to Your Watchlist Right Now

Disclosure: The author is not a licensed or registered investment adviser or broker/dealer. They are not providing you with individual investment advice. Please consult with a licensed investment professional before you invest your money.

Learn how to diversify and hedge your long-only stock portfolio. We’ve partnered with Tim Thomas to give you the opportunity to sign up for a free insight into the Swing Trading 101 program. The program has been developed over thousands of hours of trading over hundreds of thousands of dollars across stock, commodities, options, and cryptocurrencies. It’s designed to empower you to take a unique but strategic approach to the markets. Learn more about swing trading.

Tim Thomas has investments in real estate.

This post was produced by Sure Dividend and syndicated by Wealthy Living.

Featured image credit: Shutterstock.